I profoundly believe that the historical events hold myriads of lessons for us to learn from. Given the current economic scenario where it seems that the writing is on the wall and the economy is going to go in a recession, possibly a depression, it made sense for a complete finance tyro like me to try to understand what exactly happened in the global recession of the 2008 and try to procure some learnings from it.

What exactly was the “crisis”?

Preluded by financial institutes issuing subprime mortgages in big numbers, the housing prices sky-rocketed in the US due to abundance of the capital to finance such high prices. This soon led to the burst of the “housing bubble” and the prices of the real estate the house owners owned reached unprecedented lows. In many cases the mortgage was even higher than the actual value of the real estate which made the house owners walk away from their mortgages.

Since people were not paying their mortgages, the value of the mortgage-backed securities held by the investment banks like Lehman Brothers, Merrill Lynch, declined sharply in 2007-2008. Banks suddenly found themselves in debt and out of cash, some got bankrupt and some had to wail for a federal bailout.

With banks unable to lend money for credit and business loans, people down on savings and busy paying mortgages and unable to spend money, the economy went into a recession. People were laid-off, industries got shutdown, and unemployment rose to new highs.

This protracted for about 19 months. Stocks fell to their lowest, over thirty million people lost their jobs, national debt levels rose and costed the world 10s of trillions of dollars. It was a very very expensive crisis.

And it was not an accident. Executives and employees of the financial institutions made crazy amount of money as the world economy went for a toss.

How we got here?

Traditionally, investment banks got money from their partners and partners cared for their money.

Also they were tightly regulated to not let them speculate too much the with partners money.

In 1980s IBs exploded as they went public giving them hug amount of public shareholders money.

People on the wall street made a lot of money and started thinking that they earned it because they were smart.

With the start of deregulations, IBs started doing lots of fraud and money laundering to make their books look good and made hefty money in the form of bonuses.

There is a general trend that the financial industry has a certain level of criminality baked into it. It’s fundamentally different from the high-tech industry for example, where I work for instance. In the tech industry, the value creation is driven by creating something new, finance industry makes money by funnelling capital from one place to another and taking their cuts.

The securtization food chain

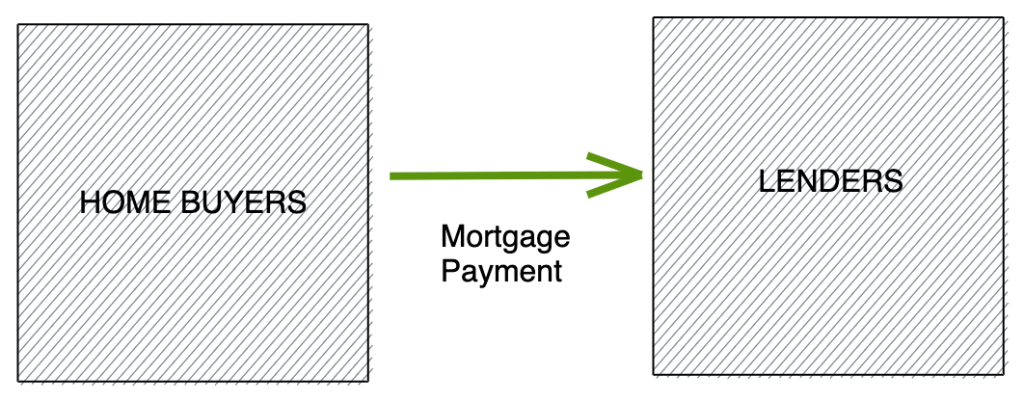

Traditionally, when a home owner sought a loan, the lender cared a lot if his money will be payed back or not. This kept sub-prime loans in check.

In the new securtization system, this was simply not true. The people who lent mortgages were no longer interested if you can pay them back.

The lenders sold their mortgages to investment banks. The investment banks combined thousands of mortgages and other loans including car loans, student loans and credit card debt to create complex derivatives called “Collateralised Debt Obligation” or CDOs. Investment banks sold these CDOs to investors all over the world.

Now when people payed mortgages the money went to the investors all over the world. Investment banks payed the rating agencies to evaluate the CDOs which gave them AAA rating which means as safe as a government security, the highest investment grade possible.

This system was a ticking time bomb. The lenders no longer cared if the borrowers could pay, and they started giving riskier loans. The investment banks did not care either, the more CDOs they sold the more money they’ll make. The rating agencies which were paid by the investment banks also had no liability if their rating was proved wrong.

With no regulatory constraints this system started pumping out more and more loans which started the subprime mortgage crisis. The numbers of loans issued in 2000 to 2003 nearly quadrupled.

Investment banks actually preferred subprime loans as they carried higher interest rates.

These loans were being given to borrowers who simply couldn’t pay them back.

And I think we all can read the signs. Such abundance of loans set the housing prices to sky-high and created the “Housing Bubble”.

The Bubble

With loans being easily available in the market, the prices of houses sky rocketed. Between 1996 and 2006, the house prices effectively doubled. This sharp increase in prices in retrospect did not make any sense at all.

Goldman Sachs, Bear Stearns, Merrill Lynch, Lehman Brothers all contributed to this impending disaster. The lending of subprime loans increased from 30 billion dollars to 600 billion dollars in a span of 10 years.

Conspicuously, as the books of these investment banks moved more money the bankers made huge amount of money.

Many people saw this free floating availability of capital in the market as loans a sign of a prospering economy and investment bankers continued to borrow money to create more loans.

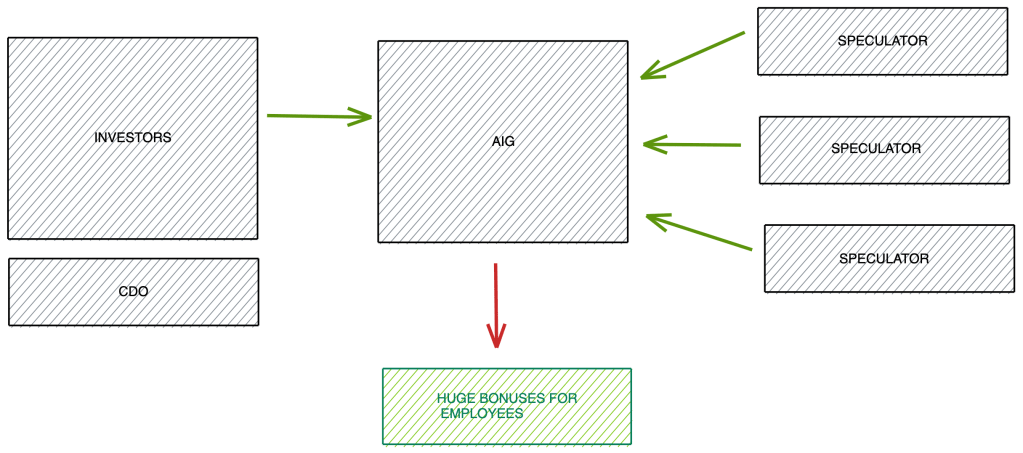

But there was another time bomb ticking, the largest insurance company in America AIG.

AIG offered insurances of the CDOs that the investors were buying in exchange of quarterly premiums payed by the investors to AIG, these were called Credit Default Swaps.

But unlike regular insurances, speculators could also buy CDS for CDO that they did not even own

Imagine 50 more people other than you who were just “speculating” your house buying insurance for it. Yes the insurance company gets more premium, but if your house burns down, the insurance company has to pay 50X more payouts.

And again because of poor regulations, AIG did not have to put money aside to pay these buyers of CDS in case the CDOs they have insured went bad. AIG instead gave its employees huge bonuses as they sold more CDS.

Unfortunately for AIG the CDOs insured consisted of large numbers of subprime loans issued by investment bankers. They were bound to fail, and AIG was sitting on time bomb created by itself.

But still why will people do this? Why will people issue loans which they know are risky? Well the root cause of the incentive structure of the financial industry. Raghuram Rajan, in his paper titled “HAS FINANCIAL DEVELOPMENT MADE THE WORLD RISKIER” pointed that bankers made huge amount of bonuses based on short term profits, but introduced no penalty for later losses. He argued that these incentives encouraged bankers to take risks that might eventually bankrupt their own firm.

The avarice bankers were given an option that they can make a million dollars in bonus by risking someone else’s money, will you take the bet? They did take the bet and the million dollars.

Well, who doesn’t like living a luxurious lifestyle, private jets, yachts and the beach house.

The Crisis

There were definite signs that inflated appraisals, documentation frauds, rating frauds etc were leading us towards the burst of the bubble. But the question was how pervasive were they?

But even as the top investment bankers kept denying the fact that there was any problem in the system, the tsunami had already hit the economy.

Within a week in September 2008, Bear Stearns, Freddie Mac, and Lehman Brothers collapsed after declaring huge losses in billions. The investment banks were sinking one after the other and the stability of the global financial system was in a great jeopardy.

In the same week AIG owed 13 billion dollars to its customers for the credit default swaps and it did not have the money. Two days later it was taken over by the American government.

All of the financial system froze up, people had their assets locked up with the now bankrupt institutions and they couldn’t get them out. People were laid-off, the credit system collapsed and nobody could borrow any money.

Later the American government had to sign a 700 billion dollars bailout bill costing tax payers huge amount of money. Meanwhile Goldman Sachs made 60 billion dollars against the credit default swaps it had bought from AIG.

The stocks continued to fall, unemployment rose to 10% and sales plummeted. And as it happens in most crisis, the poor were hit the worst. They lost their jobs with no substantial savings and no availability of credit in the market. Construction halted, sales dropped, factories shut down, there were just no jobs out there.

The Aftermath

The men who destroyed their own companies and plunged the world into a crisis walked away from the wreckage with their fortunes intact. Top executives at investment banks made billions of dollars between 2000 and 2007.

Even after the meltdown the financial industry was not remorseful and fought the regulations being put in place. America also lost its one sided dominance over the global economy, with core poorly managed American companies losing to its competitors across the globe.

There is a saying that the government is run by the Wall Street, and it does seem to be true to some extent. Major executive bankers were all consultants and advisors to the US government and passed laws to benefit the riches.

Also over time, American cost and quality of living increased as well and people responded to it in two ways.

– By either working more hours.

– Or taking credit and loans.

The markets eventually stabilised in 2011 but there was permanent damage. The median household income in US dropped from 110K USD in 2005 to 68K USD in 2011. The income inequality also increased, with riches making substantially more than the middle class.

Conclusion

The root cause of the crisis can be interpreted as the greed of the financial industry and them turning their back on the society. The top execs making millions of dollars a year thought it was okay to make more fortunes by risking the pension funds of families making less than 10k USD a year.

A needless abundance of loans triggered the sky-high housing prices bubble, and when it burst it took down most investment banks, but the bankers had already made their fortunes.

The road to recovery was not easy and took over 19 months for the markets to stabilise.

The same financial industry and people still hold prominence. They still consider that what they do is too complex for the others to understand and they keep telling the world that it’ll not happen again.

Learning about the crisis definitely made me more paranoid about the bubbles that we end up creating. Whenever we milk a cow way too much, it’ll create a bubble with inflated monetary benefits for the small segment of people who are part of it. They might think that they deserve this because they are “smart”, but it is far from the truth. They are just fortunate to be on the other side of the table.

Also I’ll be more skeptical about taking any form of debts. The idea of taking huge student loans that you cannot afford to fund education to get jobs, seems like a broken system, especially in the economic conditions that we are about to witness.

Detecting bubbles early is also important. I am no pundit here, but where ever there is mindless crowd rush and you can’t seem to logically justify, it’s better to proceed with skepticism.

References

https://www.imdb.com/title/tt1645089/

https://en.wikipedia.org/wiki/Financial_crisis_of_2007%E2%80%9308

https://en.wikipedia.org/wiki/United_States_housing_bubble

Leave a comment